RISK ANALYTICS CONSULTANCY

Consortia Solutions International Private Limited consulting services and solutions revolve around the key risk estimations and risk management challenges faced by corporations worldwide.

Effective risk management depends on accurate risk quantification. It is extremely difficult to design a sustainable and successful risk management strategy without first identifying, measuring, analyzing and understanding the existing and emerging risks that impact your business.

Consortia Solutions is an international firm providing consulting services in the fields of predictive risk analytics and decision modeling. With the help of our globally experienced team, we strive to stay on the cutting edge of quantitative modeling and analytical methods to provide our corporate clients and research partners with the most current and sound analytics to their decision questions.

Our highly specialized team of professionals uses post-modern data analytics tools and estimation techniques; and combines it with our global knowledge of risk management and regulatory issues to simulate likely scenarios and predict future events. As an outcome, we help our corporate clients manage risk efficiently throughout the enterprise, improve financial and operational performance, reduce cost and increase profits.

IFRS 9 – SOFTWARE AND EXCEL BASED MODELS

BACKGROUND

- Post 2008 financial crisis, regulators around the world realized that history based accounting standards can be extremely misleading and a paradigm shift in accounting methodologies is needed.

- In July 2014, IASB issued IFRS 9 standard which replaced existing IAS 39 provisioning method. The IASB stated that the IAS 39 incurred cost method leads to delayed recognition of credit losses, thus a forward looking approach is being introduced.

- IFRS 9 became effective worldwide on Jan 2018 and has since then posed huge challenges for accounting firms, auditors and corporations who were neither used to deal with such predictive analytics nor qualified to do so.

PROVISIONING UNDER IFRS 9

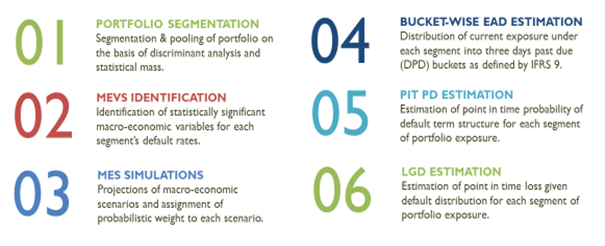

- Incurred Loss Provisioning Method under IAS 39 has been replaced by Expected Loss Provisioning Approach of IFRS 9 where provisions are taken upfront and Expected Credit Loss (ECL) is estimated as a product of EAD, PD and LGD.

- Definition of EAD is different for each of 3 buckets, term structure of applicable point in time PD is also different for each of 3 buckets of EAD, and LGD is estimated differently for collateralized and non-collateralized exposures.

OUR ECL Estimation Methodology

HOW IS IT DIFFERENT FROM BASEL?

HOW IS IT DIFFERENT FROM RATING MODELS?

MARKET RISK ANALYTICS

Our post-modern copula based statistical models assist our clients to accurately measure and monitor market risk & stressed losses.

Market risk refers to the risk of losses in a firm’s trading book due to changes in equity prices, interest rates, credit spreads, foreign-exchange rates, commodity prices, and other indicators whose values are set in a public market. To manage market risk, firms deploy a number of highly sophisticated mathematical and statistical techniques. Most popular among these is value-at-risk (VAR) analytics, which over the past 15 years has become established as the industry and regulatory standard in measuring market risk.

With time, firms need more efficient, versatile and highly functional analytics tools to address new, complex issues related to market risk. Market risk analytics involve a comprehensive set of integrated, scalable and productive solutions for wide-range risk management across various verticals of asset classes.

Risk analytics basically help organizations realize the existence of risks lying under business activities – by facilitating enterprises to identify, determine and manage their company risk. In lieu of this, the pressing need for risk analytics is going to increase across industries in the coming few years. New developments, like real-time risk analytics, which is an advanced form of traditional risk analytics process that estimates risk on a real-time basis, are influencing the entire market, while accentuating its mitigating abilities.

Our globally experienced team has been providing risk analytics and advisory services for past 25 years. We are a group of senior professionals, each with decades of direct market experience that includes trading, managing risk, working with regulators and serving on boards. We also specialize in derivatives, asset-backed securities, mortgage products (Agency and private label MBS, CMOs, and whole loans), structured finance and other complex financial products and strategies. We assist our client in advanced VaR based modeling, EVA modeling, tail loss estimation, development of Copula models, and neural simulation models for the estimation and risk management of equity, interest rates, commodity, foreign currency and derivatives portfolios.

CREDIT RISK ANALYTICS

Given the on-going turmoil in credit markets, a critical re-assessment of current capital and credit risk modeling approaches is more than ever needed.

Credit risk analytics aim to discriminate obligors and/or exposures in terms of default (PD), loss (LGD) and exposure (EAD) risk. However, losses need to be absorbed by capital in an absolute way! Hence, we aim to develop calibration procedures that come up with optimal cardinal measures of risk taking into account both past experience and future expectations. Therefore we identify which statistical technique works well on a time series of historical credit risk data and how survival analysis can be used to work with different time horizons including both point-in-time (PIT) and through-the-cycle (TTC) calibration.

Our team consists of experienced members who are expert in developing and implementing accurate and robust PD, LGD and EAD models for corporate, small and medium enterprises (SME) and the consumer sectors. This experience includes providing credit scoring such as application scorecard, behavior scorecard and collection scorecard for all consumer lending products, such as credit cards, installment loans and mortgages. With many successful assignments providing IRB approach and risk scoring to international and regional banks, we have deep industry insight and a broad array of industry benchmarks to support such initiatives.

Our services include provision of credit risk management, credit risk rating and support for underwriting, building scorecards for credit decisions, PD modeling, credit VaR modeling, periodic portfolio review and portfolio management functions, borrower financial and credit analysis and fraud analytics.

OPERATIONAL RISK ANALYTICS

Operational risk management (ORM) has long-been an imperative in the financial services sectors, due in large part to regulatory requirements and oversight. Yet the immaturity of ORM has been demonstrated, time and again, by high-profile instances of operational risk failures impacting the largest financial institutions.

Driven by new regulation, banks are soon expected to adopt a standardized measurement approach to operational risk that should enable them to model operational risk scenarios, analyze historical losses and predict future events more effectively.

The new Basel consultative paper on the standardized measurement approach (SMA) turns on its head the traditional ideas about why a bank would devote resources to operational risk capital modeling and evaluate business performance based on a return on capital measure. This methodology creates more meaningful operational risk analytics, including scenario analysis of top risks; scenario analysis based on external loss events; loss forecasting; and greater reliance in analytics on qualitative inputs such as audit scores, metrics and RCSA results. Moreover, this put greater focus on analytics will enhance the soundness of the control environment, including evaluation of control tests for control failures associated with large losses and near misses.

A pre-requisite to meaningful operational risk analytics is a data model that allows linkages between operational risk events, risk assessments, metrics and scenarios with other data objects – such as audits, control tests, vendor risk assessments, IT risk assessments and the output of other business and functional groups. To support valuable risk analysis, many are turning to advanced analytics that can help a firm streamline and automate its risk and control assessment processes; enhance collaboration across the three lines of defense; and, ultimately, gain a clearer view of operational risks across the enterprise.

We provide analysis of operational risk data and predictive analytics built on an industry leading reporting and business intelligence platform through pre-built dashboards, charts, and reports to help strengthen a financial organization’s ability to contain losses. Financial institutions can now unify risk and compliance to provide a holistic view to senior management. These advanced analytics also gives firms the ability to build many-to-many relationships across data objects, which allows for greater transparency in the relationship between risk assessments, risk events, metrics and scenario analysis.

Through these detailed analytics, organizations can analyze and compare assessment scores for all interlinked and interconnected risk disciplines against the firm’s risk appetite on a single dashboard, helping identify areas of weakness and vulnerability to different types of losses. Senior management can now be alerted to evolving situations requiring intervention through time-series analyses of performance trends and automated notifications.

Our services specific operational process reviews, risk management analysis and self-assessments (RCSA), heat charts, credit and collateral management, data integrity, analysis and validation, and business continuity planning.

MODEL VALIDATION

The critical role played by internal models, industry leading practices and regulatory requirements dictate that financial institutions implement an independent model validation process to assess the quality and accuracy of their internal models.

Independent validation of internal statistical models is in increasing demand under Basel framework. Firms worldwide need to invest and implement a strong mechanism via systems to authenticate the precision and reliability of rating systems, processes, and the appraisal of all relevant risk components. In addition, firms must also demonstrate to regulators the completeness of their internal models validation process.

While the various aspects of model quality can be assessed with complicated quantitative procedures, qualitative judgment is essential to guarantee that the financial institutions are using the correct model. As a consequence, the efforts involve a combination of in-depth knowledge in analytical validation techniques as well as banking industry practices.

We add value by helping our clients to implement a model validation process. Our services include qualitative and quantitative model validation analytics to test the mathematical integrity and conceptual soundness of estimation models in line with global estimation standards. We provide:

Initial model validation: Review of the model development, the processes and the execution of the model.

Ongoing model validation: Ongoing validation of rank-order performance using industry wide standard metrics.

REGULATORY AND INTERNAL COMPLIANCE

Being and staying compliant is a constant challenge. New laws and regulations are constantly being introduced or changed. The ability for the organization to interpret these regulations well and to operationalize and sustain compliance practices requires diligence, an understanding of their relevancy to the business, and continual communication.

Today’s complex regulatory environment is presenting many difficult challenges to financial institutions of all sizes. Increased regulation is consuming unprecedented resources for firms and requiring high levels of expertise. We are here to help with a full range of regulatory compliance services that are designed to help you cope with today’s multifaceted regulatory challenges. We work with our compliance clients to prevent potential problems, correct existing issues and proactively provide guidance to efficiently stay ahead of a rapidly changing regulatory landscape.

We provide services for the periodic review, monitoring, and determination of the firm’s compliance with the laws and regulations subject to regulatory scrutiny. We also provide consultation and staff training in those areas in which compliance may not be considered satisfactory, while ensuring that the institution has established appropriate procedures and controls for ongoing compliance with those regulations.

Additionally, our team of experts provides advanced quantitative services in following

- Regulatory compliance analytics: This includes Basel II and Basel III related analytics required by the regulators including CAR estimations, ICAAP modeling, ILAAP modeling and ICLAAP modeling.

- Capital planning and predictive analytics: This includes optimization analytics, pricing analytics, client service analytics, capital planning, loss forecasting, model development & validation, stress testing, and reporting of risk to enable our clients take smarter decisions and understand higher outcomes.

- Treasury risk analytics: This includes mark to market valuation models, cash flow at risk (CaR) modeling, VaR modeling, sensitivity analysis, yield curve modeling, counter party risk analytics and duration/modified duration estimations.

- Derivative valuation & pricing: This includes point in time estimation of derivative portfolio using real time simulated analytics for futures, forwards, options, swaps and exotic/combo derivative baskets.